ADVERTISEMENT

Case Study: Cardiac Rhythm Management Purchasing

Cardiac Rhythm Device Management (CRDM or CRM) products are a big part of the economic and clinical operation of cath and EP labs. CRM products include permanent pacemakers, implantable cardioverter-defibrillators (ICDs), cardiac resynchronization  therapy (CRT-D or CRT-P) devices, and implantable loop recorders. These devices are typically implanted in the chest to record and/or regulate the heart rate.

therapy (CRT-D or CRT-P) devices, and implantable loop recorders. These devices are typically implanted in the chest to record and/or regulate the heart rate.

Cardiac Partners has entered into dozens of CRM contracting arrangements over its 30+ years of developing and operating cardiac cath labs. Contract negotiations and final deal structures have touched on many strategies described below. This article will review some circumstances unique to the CRM market and will provide a case study of one facility’s successful approach to CRM contracting. Thank you to my friends and colleagues on both sides of these negotiations for your suggestions and contributions to this article.

Why is CRM Purchasing Important to You and Your Facility?

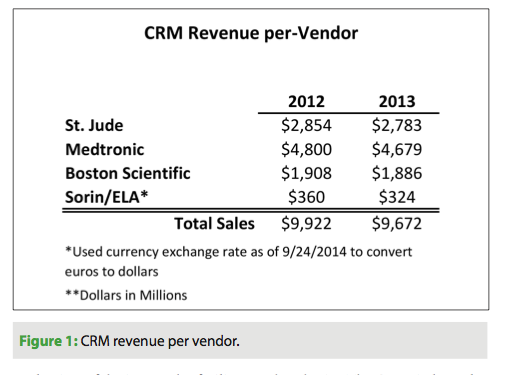

The CRM industry is huge. In 2013, CRM device revenues totaled $10 billion according to financials reported by Medtronic1, St. Jude Medical2, Boston Scientific3, and the Sorin Group4. Please refer to Figure 1 for a summary of per-company CRM revenues. The figure shows that Medtronic, St. Jude Medical, and Boston Scientific are the three largest players. How important is CRM purchasing to your facility? From my facility management experience, CRM device purchases make up approximately one-third of the total cost of supplies and implantable devices for a complex cath/EP lab. Do you, or does someone in your facility, spend one-third of their time understanding the purchasing process, and managing that process for the best outcome? What is the best outcome? Perhaps the lowest price? The best technology? The best service to the physician? The best service to the patient?

Multi-Party Transaction

For typical purchase transactions outside of healthcare, there are two parties: the buyer and the seller. For CRM purchasing, like most hospital purchasing, there are multiple parties. The parties include the CRM vendor, the physician, the hospital, and the patient. The CRM vendor is clearly the seller, but who is the buyer? The patient is the ultimate beneficiary, but rarely selects the device. The hospital buys the device, but rarely determines when a device is necessary or selects the device. The doctor is typically the primary decision maker. He or she decides when a device is necessary, and then selects the appropriate device for the patient’s clinical condition. The hospital’s role, exercised through supply chain managers, value analysis, or similar processes, usually takes the form of a single determination that a vendor (or specific product) is either “in” or “out.” If “in”, then a doctor can choose that vendor or device. If out, then that device or vendor is not available for selection by the physician. Thus, the hospital’s role is usually that of a blocker. The hospital can block a selection, but does not make the selection.

Typical CRM Sales/Implant Process

At most hospitals, the sale and implant of a pacemaker might look something like this. A physician sees a patient in his or her office or clinic, and determines that a pacemaker is needed. The physician communicates to office staff to schedule the procedure and contact a specific vendor for that procedure. At the appointed date and time, the physician, patient, and vendor are all at the facility for the implant. The vendor may perform all or many of the following: bring a selection of devices to the facility; make product selection recommendations to the physician; meet with the patient to help with pre- or post-implant education; enroll the patient in remote monitoring; assist with programming the device at the time of implant; pair the device with the remote monitoring base station; and otherwise assist with the process. In many areas, the CRM device representative will provide additional post-implant support in areas such as after-hours support, device clinic support, programming, and related device follow-up. The CRM representatives work hard to become an integral part of the clinical team.

System or Line Item Pricing

Understanding device packaging strategies is another complexity that can be important in CRM contracting. Pacemakers and ICDs consist of the actual device (the “can”) and the leads which connect the device to the heart. These can be sold separately (line item pricing) or together as a complete package (a “system”). New implants are typically purchased as a system at a reduced price. The CRM industry has pushed the system approach for years, but recently seems to be relaxing that approach. We recommend eliminating “systems” from your contracts, to avoid the complexity of multiple inventory items.

Product Life Cycle

The product life cycle theory describes the various stages of a product’s life: introduction, growth, maturity, and decline.5 Items that are in introduction and growth stages offer new technologies, and sellers are able to obtain premium prices. As a product matures, and innovation slows, the technologies are commoditized. Commoditization means “to render (a good or service) widely available and interchangeable with one provided by another company.”6 Where are CRM devices in the product life cycle? The first pacemaker was implanted in the U.S. in 1960, some 54 years ago.7 Surely, pacemakers must be a mature product. Consider what has happened with bare metal and drug-eluting stents. When first introduced, stents reflected a significant technological advancement. The Palmaz-Schatz stent was the first FDA-approved stent device, and the vendor was able to charge a premium price. As other stent devices were introduced, the price per-stent dropped. Today, drug-eluting stents are a mature product, resulting in commoditization and falling prices.8 The CRM manufacturers continue to evolve products regularly with new features. By following a disciplined approach, each manufacturer introduces a “new” product periodically to avoid commodity pricing. Many electrophysiologists in my network tell me many new pacemaker features are driven by engineering capabilities rather than clinical needs. If your physicians share this sentiment, you may be able to drive down prices. On the other hand, some physicians may be drawn to revolutionary new products such as MRI-compatible pacemakers or tiny new leadless pacemakers. Whether or not your facility is able to capitalize on commodity pricing will largely be a factor of whether your physicians are convinced they need the latest innovations.

Death of the Device Salesman?

In August 2014, Modern Healthcare published an article with the catchy title, “Death of the Device Salesman?”.9 The article described how several hospitals contracted directly with manufacturers to buy orthopedic products without sales representative support. Will this occur with CRM device purchasing? At the present time, there are very few examples of reduced CRM pricing in exchange for little or no sales representative support. Each of the market conditions described above — multi-party transaction, representative’s participation in the implant process, product life cycle, and large dollar transaction — all tend to keep the CRM sales representatives gainfully employed. However, hospitals will continue to be challenged by reduced reimbursement, and vendors may decide at some point to cut sales costs by eliminating local representation. Elimination of local representation is more likely if a hospital successfully contracted with a single vendor for all implants, so the sales representative would no longer be required to assure a sale. We will go over contracting strategies in more detail below, but so far, exclusive CRM deals have only occurred for me in small communities where it was not economical for multiple companies to compete for business. The exclusive arrangement allowed for normalized prices by offering an economy of scale for the single remaining vendor.

Contracting Strategies

Typical CRM contracting strategies include: 1) Capitated, or, Pay-to-Play systems; 2) rebates based on market share or level of sales; 3) bulk or quantity purchases; or 4) limiting the number of vendors. It is common that a combination of these strategies is used at any given site. Each of these strategies is explained below.

A Capitated Pay-to-Play contract is a simple approach by which a hospital or chain of hospitals sets a capitated price per device. A manufacturer can choose to accept the proposed prices and stay “in” with that hospital or chain, or it can decline the proposal and be “out”. If out, then a physician is not able to select that manufacturer or product. There are many variations on this approach. For example, permanent pacemakers could have a three-tiered pricing structure for Premium, Advanced, and Standard, or a two-tiered system such as Special and Regular. The Capitated Pay-to-Play strategy is most commonly followed at a large system or hospital chain level, and establishes a baseline of prices for hospitals within the system. Individual hospitals, or subsets of hospitals within the chain, can then use additional contracting strategies below.

Market share is defined as “the percentage that a company has of the total sales for a particular product or service”.10 For example, the hospital may use 20% vendor A, 30% vendor B, and 50% vendor C to make up the total available market (100%). A market share commitment for CRM purchases may seem simple, but there are a few unique circumstances.

Be sure that you have a clear understanding of whether your market share commitment includes new or de novo implants only, or whether it also includes generator replacements. CRM devices must be periodically replaced, usually when the battery reaches end of life. Physicians generally prefer to replace devices with the same brand. Maybe it is as simple as the comments that I have heard from several physicians, “If a device has been implanted and supported for five years or more, I hate to reward the company for its support by switching brands.” Or if a patient’s experience has been positive, then he or she may also be reluctant to change. Before entering into a market share deal, review your facility’s market share of the prior five years of implants, since that will be an excellent estimate of your future device replacements. Before making a market share commitment, be sure to: discuss the new versus replacement phenomena with your physicians; understand the past implant patterns; and be sure that you have their support to achieve your commitment.

How is compliance with a market share commitment measured? Each vendor has a good understanding of its sales to the hospital, but can only estimate the other vendors’ activity. As a result, it is common for a market share agreement to require the participating hospital to periodically report the sales of all CRM vendor activity. In some circumstances, the facility is uncomfortable sharing sales information for all vendors. A simple solution is to estimate a specific level of sales for a given vendor that would achieve the vendor’s goals. The target could be expressed in terms of dollar level of CRM purchases or number of devices. If the level of sales approach is used, then the facility no longer needs to report purchases made from other vendors.

Market share or level of sales agreements are often tied to periodic rebates. A customer is incentivized to meet the market share commitment, but does not receive the benefit of the agreement unless the facility meets its commitment level. An alternative is to get up-front pricing based on achieving the market share, but revert back to a different price tier if the market share is not met.

Bulk purchase, sometimes called a quantity purchase, is a one-time acquisition of a large quantity of items in exchange for a reduced price. For example, a hospital may make a single bulk purchase for combination of common pacemaker and ICD products in exchange for a 10% discount. This approach offers some advantages. The hospital is not required to measure or report its CRM market share. CRM savings are clear. The difficulties with bulk purchases include: the advance purchase of an inventory of expensive items; items that are sometimes purchased as a system, but are broken down into devices and leads; and difficulty in accurately predicting future product needs.

Limiting vendors is the practice of reducing the quantity of vendors, resulting in increased market share per vendor. The CRM industry is dominated by three large vendors. If a hospital or chain is able to limit itself to only two vendors, then the remaining vendors will often offer price concessions. This is often referred to as a dual vendor agreement.

Dyad Management Structure

The CRM purchasing process is unique. Many parties are involved in the transaction, and there are unique clinical decision-making steps. Physician participation and support are the key elements to success. Dyad management styles are increasingly common in healthcare due to changes in the environment. Dyad is defined as “two individuals maintaining a sociologically significant relationship”.11 Daniel Zismer, PhD, and James Bruggemann, MD define dyad in healthcare as the collaboration of qualified physician and non-physician managers.12 Improved care quality and cost reduction can be achieved from working collaboratively between the two individuals. The physician and non-physician leads have separate responsibilities, but share common goals and values. The  article, “Examining the ‘Dyad’ as a Management Model in Integrated Health Systems”, provides useful suggestions to structure and operate a dyadic system. The administrative managers should not be the sole input for supply chain management decisions. Physicians play a significant role because they ultimately choose a specific device based on service history and clinical requirements. The CRM contracting process should include physicians, administrators, and device manufacturers, because physician buy-in and compliance are key factors for successful CRM purchasing.

article, “Examining the ‘Dyad’ as a Management Model in Integrated Health Systems”, provides useful suggestions to structure and operate a dyadic system. The administrative managers should not be the sole input for supply chain management decisions. Physicians play a significant role because they ultimately choose a specific device based on service history and clinical requirements. The CRM contracting process should include physicians, administrators, and device manufacturers, because physician buy-in and compliance are key factors for successful CRM purchasing.

Case Study

A Cardiac Partners client site was approached by one of the CRM vendors to explore ways that the vendor could expand its market share in exchange for reduced prices. The first step was to understand past CRM purchasing activity and any current changes or trends in that activity. The site uses the CPLink Cardiovascular Database System® to measure and report physician supply or implantable device usage. As it turned out, the facility’s CRM purchasing pattern was already nearly a dual vendor facility, with a five-year historic market share of: Vendor One – 35%; Vendor Two – 60%; and Vendor Three – 5%. As explained above, the five-year baseline is a good predictor of device replacements in future years. The data indicated a shift toward Vendor One in the most recent 12 months, with a rolling 12-month market share of: Vendor One – 55%; Vendor Two – 44%; and Vendor Three – 1%. Approximately 60% of all implants were new implants, and 40% were replacements. The facility had been approached by Vendor One,  requesting a 75% market share commitment. In light of the preference to use the original manufacturer for device replacements, 24% of all device purchases were already spoken for (40% replacements x 60% non-Vendor One five-year baseline = 24%). We discussed these figures with the physicians, who agreed that a 75% market share of all CRM devices was not possible, but they did believe that a 75% share of new implants could be achieved.

requesting a 75% market share commitment. In light of the preference to use the original manufacturer for device replacements, 24% of all device purchases were already spoken for (40% replacements x 60% non-Vendor One five-year baseline = 24%). We discussed these figures with the physicians, who agreed that a 75% market share of all CRM devices was not possible, but they did believe that a 75% share of new implants could be achieved.

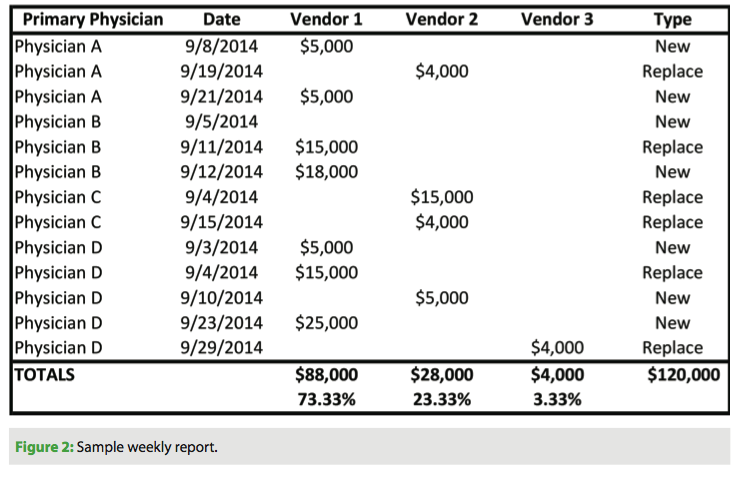

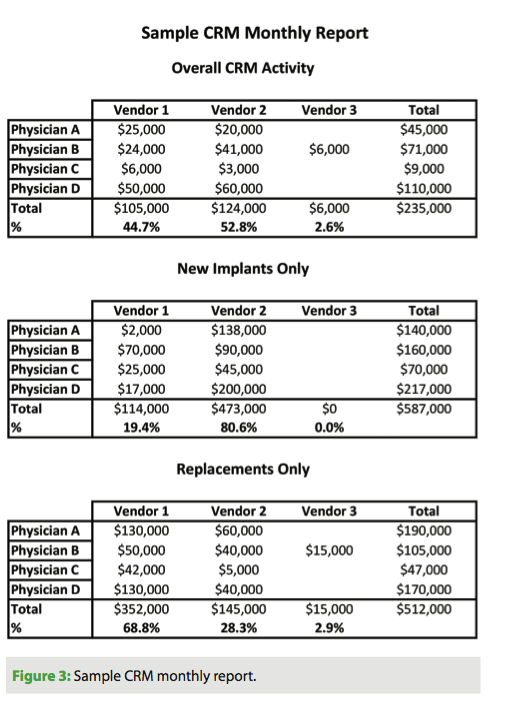

The first month’s compliance was an astonishing 85% Vendor One implants of new devices. The next month increased to 88%. Figures then tapered down to 68% in the third month. Clearly, we needed to take action. The initiative had lost its momentum. Our physician dyad leader suggested that we routinely circulate a CPLink-generated report to each of the physicians; this report showed the individual implant figures of each physician. Figure 2 is a sample weekly report. The physicians tend to have a good sense of the number of CRM device implants they perform each week, but are not aware of the dollar cost of each device. In this case, the market share was measured in terms of dollars. The weekly report had the desired effect, and the fourth month share reverted back to 81%. Another useful report, the sample monthly report (Figure 3), shows overall CRM activity at the facility, new implant activity to measure per-physician and per-vendor market share, and replacement activity.

TakeAways

Try this simple three-step method of CRM contracting at your facility. First, collect baseline data. CPLink Cardiovascular Database System® provided us the five-year baseline data to project replacement devices. Second, discuss the data trends with your  doctors and develop a plan that they will support moving forward. Discuss alternative contracting strategies with your physicians. Calculate the total cost savings to the hospital. Do you have an effective dyadic structure? Consider offering the physicians some benefit if they meet the goals. Perhaps earmark the savings for pet projects such as staff training or new capital improvements. You need physician support and buy-in to have success. Third, provide timely feedback to the physicians. We use CPLink reports (Figure 2) to provide feedback to the physician decision-makers — a necessity, especially when the rebate arrangement relied on whether or not the 75% hurdle was achieved in each calendar quarter.

doctors and develop a plan that they will support moving forward. Discuss alternative contracting strategies with your physicians. Calculate the total cost savings to the hospital. Do you have an effective dyadic structure? Consider offering the physicians some benefit if they meet the goals. Perhaps earmark the savings for pet projects such as staff training or new capital improvements. You need physician support and buy-in to have success. Third, provide timely feedback to the physicians. We use CPLink reports (Figure 2) to provide feedback to the physician decision-makers — a necessity, especially when the rebate arrangement relied on whether or not the 75% hurdle was achieved in each calendar quarter.

Our hospital system is currently considering a system-wide dual vendor agreement, which will likely be combined with individual hospital market share commitments. I hope that you find this article informative as your system and/or hospital considers its options for CRM contracting. I welcome your comments and ideas.

The author can be contacted at jcarroll@cardiacpartners.com, or at www.cardiacpartners.com.

Disclosures: The author has no conflicts of interest to report regarding the content herein.

References

- Form 10-K, Medtronic, INC. April 26, 2013. Available online at https://annualreport.medtronic.com/wcm/groups/mdtcom_sg/@mdt/@corp/documents/documents/10k_report_2013.pdf. Accessed September 28, 2014.

- 2013 Financial Report. St. Jude Medical. Available online at https://sjm.com/~/media/SJM/Annual%20Reports/2013/2013_FinancialReport.ashx. Accessed September 28, 2014.

- 2013 Online Annual Report. Boston Scientific. Available online at https://www.bostonscientific.com/templatedata/imports/HTML/2013ar/corporate-information.html. Accessed September 28, 2014.

- 2013 Annual Report. Sorin Group. Available online at https://www.sorin.comhttps://s3.amazonaws.com/HMP/hmp_ln/imported/roles/9/files/SORIN%202013%20ANNUAL%20REPORT(3).pdf. Accessed September 28, 2014.

- Product Life Cycle. Inc. Encyclopedia. Available online at https://www.inc.com/encyclopedia/product-life-cycle.html. Accessed October 7, 2014.

- Commoditize Definition. Meriam-Webster. Available online at https://www.merriam-webster.com/dictionary/commoditize. Accessed October 3, 2014.

- Beck H, Boden WE, Patibandla S, et al. 50th Anniversary of the first successful permanent pacemaker implantation in the United States: historical review and future directions. Am J Cardiol. 2010;106:810-818.

- Serio, Adele. Cost Reduction: The Value of Partnerships in the Medical Marketplace: What happened after one institution committed to a single vendor for coronary artery drug-eluting stents. Cath Lab Digest. March 2014. https://www.cathlabdigest.com/articles/Cost-Reduction-Value-Partnerships-Medical-Marketplace-What-happened-after-one-institution-c. Accessed September 30, 2014.

- Lee J. Death of the Device Salesman? Hospitals train staff to take over OR role of helping surgeons. Mod Healthc. 2014;44:16-18.

- Market Share Definition. Meriam-Webster. Available online at https://www.merriam-webster.com/dictionary/market%20share. Accessed September 31, 2014.

- Dyad Definition. Meriam-Webster. Available online at https://www.merriam-webster.com/dictionary/dyad?show=0&t=1412198307. Accessed October 1, 2014.

- Zismer, Daniel K., PhD, and Brueggemann, James, MD. Examining the “Dyad” as a Management Model in Integrated Health Systems. January/ February 2010. Northern New England Association of Healthcare Executives. Available online at https://nneahe.ache.org/Documents/Examining%20the%20Dyad%20as%20a%20Mngmt%20Model%20in%20Integrated%20Health%20Systems_DZ%20and%20J.Brueggemann%20Article.pdf. Accessed October 2, 2014.